Article Links

Timeline

When will this be released?

Release Date, 12/12/2024 from 5:00 – 6:30 pm PDT, PST.

Is there downtime for this release?

No.

Payroll

IRA Secure 2.0 - Increased catch-up limits for individuals ages 60-63

With this release, we've added a feature that increases the following qualified plans’ catch-up limits for individuals aged 60-63.

- SIMPLE IRA

- 401(k)

- 403(b)

- 457(b)

- Roth 401(k)

- Roth 403(b)

- Roth 457(b)

Previously, only individuals aged 50 and above could increase catch-up contributions using the benefits module's catch-up parameter.

This new global option introduces the following:

- Enhanced catch-up limits per Section 109 of the SECURE 2.0 Act, effective January 1, 2025.

- No changes to the catch-up contributions for those aged 50+ on qualified plans; the tax engine will continue supporting these.

Published in the Internal Revenue Bulletin 2024-2:

Section 109 of the SECURE 2.0 Act amends section 414(v) of the Code to increase the annual limit on catch-up contributions, beginning with the 2025 taxable year, for individuals between ages 60 and 63. For non-SIMPLE plans, the increased limit is the greater of $10,000 or 150% of the regular catch-up limit for 2024, indexed for inflation. For SIMPLE plans, the increased limit is the greater of $5,000 or 150% of the regular catch-up limit for 2025, indexed for inflation.

Plan Implications

SIMPLE IRA

The engine enables individuals aged 60-63 to increase their catch-up contributions to the greater of $5,000 (adjusted for inflation) or 150% of the standard catch-up limit for 2025. Given that 150% of the $3,500 standard limit equals $5,250, which exceeds $5,000, the increased catch-up limit will be $5,250.

401(k), 403(b), 457(b), Roth 401(k), Roth 403(b) and Roth 457(b)

The engine will allow individuals between ages 60-63 to increase contributions to the greater of $10,000, indexed, or 150% of the regular limit on catch-up contributions, if higher (150% x $7,500 standard catch-up limit = $11,250, which is greater than $10,000; so, the increased catch-up limit will be $11,250).

Value

This feature allows Payroll Administrators to offer the new Secure 2.0 catch-up contributions.

Audience

Payroll Administrators.

Audit Logs

With this release, we’ve introduced a new feature that allows Payroll Administrators to audit any changes made to an employee’s Tax Setup or Direct Deposit parameters.

Value

This new feature helps Payroll Administrators to identify/audit their employee’s Tax Setup or Direct Deposit parameter changes. This enhancement is especially helpful if there has been a change in the calculated tax or direct deposit amount for an employee.

Audience

Payroll Administrators.

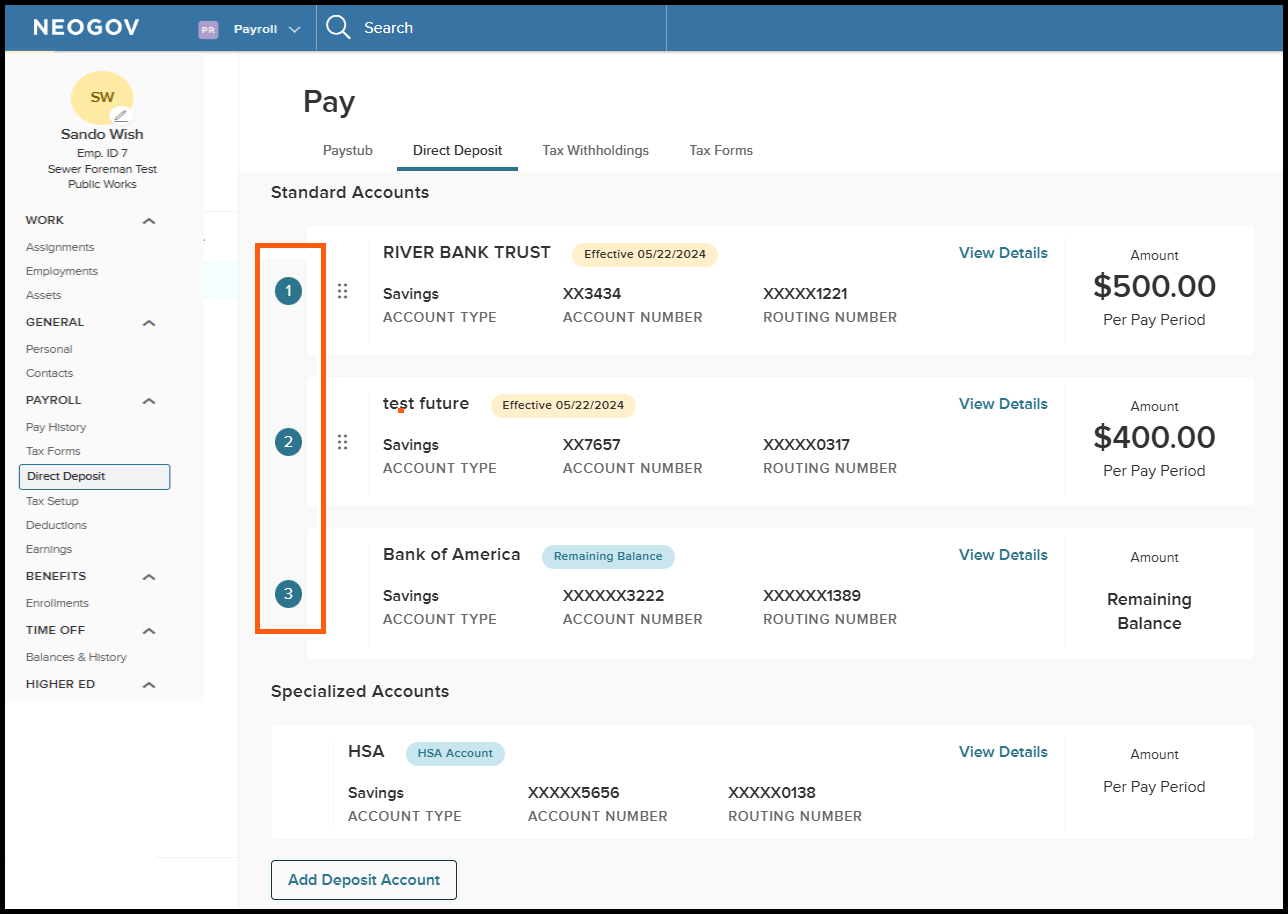

Direct Deposit UI/UX Changes

With this release, we have improved the layout of the Direct Deposit accounts by adding numbered ordering.

Value

You can now easily view how your accounts handle Direct Deposits and dynamically rearrange their order. The only exception is the Health Savings Account (HSA), where you can maintain just one account at anytime.

Audience

Payroll Administrators.

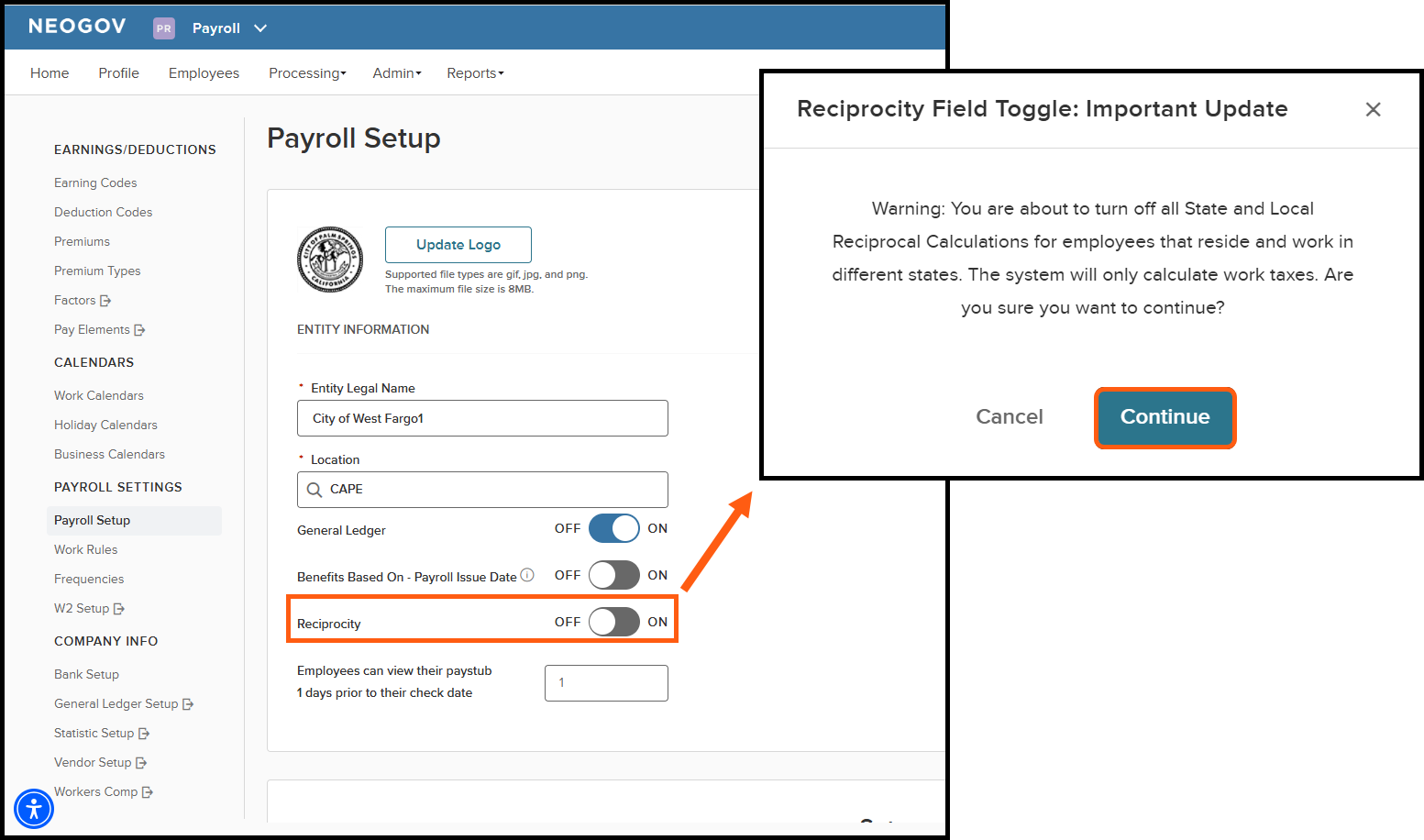

Payroll Setup - Reciprocity

In this release, we've upgraded the Reciprocity section in Payroll Setup to a toggle instead of a list of values. By default, the toggle is set to ON, enabling NEOGOV to accurately perform the necessary reciprocal calculations when an employee lives in one state and works in another.

IMPORTANT: This toggle should be set and kept the same throughout the year, as it can impact tax withholding calculations. When toggled to OFF for Reciprocity, the payroll engine will only withhold taxes for the non-resident or employee's work state.

NEOGOV generates the following update when you’ve set the toggle to OFF:

“Warning: You are about to turn off all State and Local Reciprocal Calculations for employees that reside and work in different states. The system will only calculate work taxes. Are you sure you want to continue?”

Prerequisite Setup

Each year, for states with a Non-Resident Certificate form, an employee is asked to fill in relevant information from the previous year. Non-resident certificates are forms used to indicate that an employee living in one state and working in another state that has a reciprocal agreement with their resident state has chosen to be exempt from withholding income tax in their work state. The employee completes the nonresident certificate and files it with their employer, indicating that the employer should not withhold tax on wages earned in the work state.

For reciprocal calculations to work properly within the payroll system, select the Non-Resident Certificate Filed option for the employee's non-resident/work state. You can find this option in Payroll > Tax Setup > Additional Parameters > State Reciprocity > Non-Resident Certificate Filed. The Non-Resident Certificate Filed option enables the payroll engine to calculate the resident withholding instead of the non-resident/work state withholding tax.

Value

Allows Payroll Administrators to know confidently that the reciprocal calculations are occurring correctly. In many cases, it is advantageous to the employee to have their resident state withholding to calculate rather than their non-resident or work state to withhold due to a lower tax rate.

Audience

Payroll Administrators.

Appendix: Bugs Resolved

| Scenario | Issue |

| The Tax Create PTM PayrollQuarterly Data File [UPPTMQD] expecting to use the Tax Export Code on the entity in Payroll Setup. | The Tax Create PTM PayrollQuarterly Data File [UPPTMQD] is not using the Tax Export Code on the entity in Payroll Setup. |